Legal product reviews and business guidance from industry experts.

Chapter 2/6

Creating a Long-Term Financial Strategy for Your Firm

Law Firm Finances

11 min read

Legal product reviews and business guidance from industry experts.

Chapter 2/6

Law Firm Finances

11 min read

After taking a random glance at his books, Tim realized that after five years as a law firm owner, he was nowhere close to the financial level he expected to be at by now. In fact, he was still struggling to get ahead.

Like many other business owners, Tim started a new law firm without a simple strategy in place. Unfortunately, he’s not alone.

Any healthy business, including law firms, should have a written plan to forecast revenue, expenses, net profit, and cash reserves. But this isn’t something you do just to check it off your list. It’s more important than that. This strategy is the tool you use to manage your day-to-day business so you can reach your future financial goals.

We need a solid budget in place to know how much money we’ll need to cover expenses and pay ourselves. Now, hearing the word “budget.” You may be ready to tuck tail and run. After all, the idea of creating a budget may feel overwhelming, especially if you’ve already been in business for several years. But a budget isn’t just functional—it’s a vital part of your business strategy, whether you’re starting a new firm or trying to keep your mature firm afloat.

Start your budget by putting together a spreadsheet, broken down by month. Now, you’ll do your best to predict how much income you expect to generate and how much you will spend on business expenses.

Start by estimating how many clients you’ll earn in a year, how many matters you’ll open for each of them, how much you’ll charge for each matter, and the average revenue you can expect from each. Don’t pull your hair out here—it’s only an estimate.

Next, consider expenses. How much do you expect to spend? Fixed Expenses are typically business costs that are the same each month while variable expenses vary.

You should easily know larger fixed expenses like rent and payroll. Then, fill in office expenses, internet fees, software subscriptions, bank fees, mobile phone service, website hosting…the list goes on.

Not everything within your budget is predictable. In fact, variable costs can crop up?. Variable costs don’t have fixed prices each month.

Examples of variable costs include:

There are also one-time costs that can add up quickly. One time costs—or infrequent costs—might include:

It’s smart to include anything you want or need to buy for your law firm on your budget; remember to be intentional. Set aside some of your budget for these items, so you’re prepared in advance. Don’t let a broken computer result in costly firm downtime.

As business owners ourselves, we know that business is unpredictable. That’s why we take every number on our expense side of our budget and add five-to-ten percent. We also do the same on our revenue side. This ensures we have some necessary cushion available for whatever cost or random expense comes our way.

Typically, a budget will look at a year of anticipated revenue and expenses. With a basic understanding of your annual budget in hand, you can move to longer term modeling.

First things first, you must consider where you want to be in one year, three years, and five years from now. Once you visualize those goals, you can start outlining the steps you’ll need to take to get there—the backbone of your financial strategy.

For example, do you want to double your income in the next five years? Suppose that the year 1 budget shows $250K of income. To double your income, you’d have to grow your business by $250,000 or $50,000 a year. How might you accomplish that goal? Now, you can ?walk through different options to understand the implications of each.

If your average case file generates $2,500, one option is to generate 20 additional clients each year. Do you have the current capacity to handle that many more cases? Or, would you need to invest in better technology or more staff? Would you need to up your marketing to attract more leads? If so, you’d need to add these expenses to your projections and look at how both the increased revenue and increased expenses impact your profit. Maybe, instead, you explore raising your prices or offering a different service that doesn’t require the same investment in tech or staff.

As you consider these questions, you’ll see a roadmap take shape.

Now that your annual budget and your longer financial model show you where you want to go, it is time to break those big-picture goals down into benchmarks. It’s time to define your numbers so you can start tracking them.

From the example above, you know you want to increase revenue by $250,000 over the next five years. You can create your benchmarks based on this goal by breaking down that number by year and then by month.

This will help you visualize the amount of revenue you’ll need to add each month. Using our example, we need to generate an additional $4,166 a month. With an average case value of $2,500, this means we need to add 2 more new clients each month. Benchmarks are more attainable when broken down each month and they keep you on track.

Go Deeper: Podcast Episode #357

Eavesdropping on a Financial Strategy Call with Jennifer Longtin

Listen to EpisodeMoney doesn’t grow on trees. So, where does the cash flow you need to run your business come from? There are various ways law firms cover their start-up costs and the first few months of operating costs. We detail those start-up costs in Lawyerist’s Complete Guide to Starting a Law Firm.

After that, cash will generally come from day-to-day business operations. You’ll use the money you generate from client work to fund business expenses. You need to understand lock-up to predict which money you’ll have available for your business.

Liz knew she had just completed a case that would bring in the revenue needed to pay for next month’s bills. Suddenly, she found herself halfway through next month, still without payment. Unable to pay the bills, she scrounged for cash wherever she could, making it through by the skin of her teeth.

Are you sweating yet? Sure, most of your cash flow will come from your business operations or from the money you generate from serving your clients. However, you must understand that lock-up could pose a real threat to your business. Bottom line: It often takes months to be paid after producing the work.

When that cash doesn’t arrive on time, it may leave you frantically searching the couch cushions like Liz. You may have to resort to not paying yourself or using debt capital, such as credit cards or loans. Unfortunately, this can create a financial burden on your firm and your personal life.

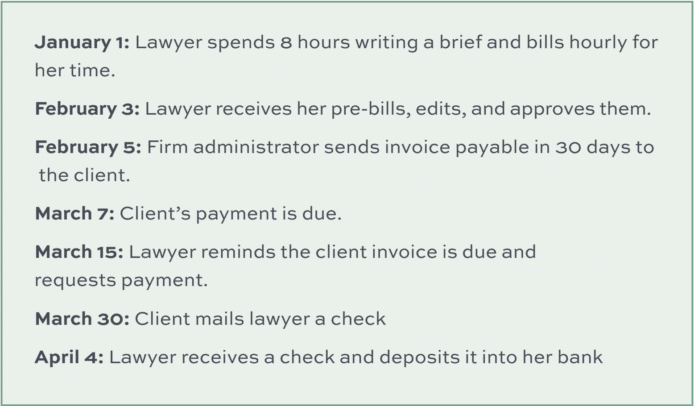

Lock-up is the time from when you perform the work to when the firm collects the money for those services. Consider this timeline:

In this example, lock-up was 93 days. Many studies estimate that law firms average between 110-140 easy worth of earnings sitting in lock-up.

The problem is that the lawyer still had to pay herself, her team, and her bills in January, February, and March, but didn’t have the benefit of the money from the work she performed on January 1 to do so. You can quickly see why lock-up can be an enormous problem for law firms.

There are ways to avoid having your cash stuck in lock-up. First, consider alternative billing arrangements. In Lawyerist’s Complete Guide to Law Firm Pricing, we break down different ways you can charge for your services. Many services, like flat fees and subscription services, allow the firm to earn and collect the fee (or a portion of it) upon engagement. As a result, the firm collects money at the beginning of rendering services instead of the end.

Alternatively, attorneys can insist that clients deposit money into their IOLTA trust accounts. Firms must establish these accounts to hold the client’s money until the attorney has earned it and can rightfully transfer the funds into her bank account. In the above example, being able to transfer funds from the trust account to the operating account on February 5 after invoicing, the lawyer would have decimated the lock-up period by 58 days.

Another option is to invoice clients in shorter intervals—twice a month—instead of monthly. Finally, firms can reduce lock-up by shortening payment terms from 30 days to “due upon receipt” and staying on top of collections. We’ll cover those in more detail in Chapter 3.

The firm’s goal should be to collect cash as soon as it can to finance ongoing business operations.

Even with the best intentions in place, businesses can find themselves short on cash from time to time. It’s a good idea to have access to cash for when you hit those speed bumps.

For most firms, it’s a good idea to have at least two months of operating expenses set aside in a cash reserve account. If your firm doesn’t have regular income (say a contingency practice), you may find you need even more set aside to pay operating expenses in between settlements.

Alternatively, you can have access to a line of credit, credit cards, and loans.

A bank or credit union typically offers a line of credit as a way for the firm to fund business expenses temporarily. It gives you access to money as you need it, and you can draw up to a maximum amount for a set period. Lines of credit are flexible, allowing you to borrow the funds you pay back continuously. You also don’t pay any interest until you borrow.

Business lines of credit are often unsecured, which means you don’t need to put forth any collateral to secure the credit. These typically come with higher interest rates, however. The saying holds true that the best time to ask for money is when you have it. It’s not a bad idea to apply for a line of credit when you don’t need it so you’ll have it available when you do.

Credit cards are like lines of credit, with a few key differences. For example, a credit card doesn’t have a draw period, so you can use it as long as the account is open. If you want actual cash in hand (like you’d receive from your line of credit), you’ll need to perform a cash advance on your card. This often comes at extremely high-interest rates, which can cost you.

Speaking of higher interest rates, credit cards come with higher rates than the other lending options listed here. With some cards, you may pay the balance off each month and avoid interest charges. That makes them an often ideal choice for day-to-day spending within your firm.

You need capital to get big-ticket items such as a new office or new technology for your firm. And if you were wondering when the long-term strategy would pop back up, it’s now. Law firms prepared for the future will forecast these large expenses ahead of time, ensuring they have access to the capital they need.

Most firms will typically distribute any profit to the partners of the firm at the end of the year to avoid higher taxes. Unfortunately, draining your firm’s bank account in this way also drains your ability to grow your firm. Smart firms will instead decide to reinvest their profits.

Budgeting is worth pushing through the discomfort and frustration. With the foundation of a financial strategy in place, we’ll show you how you can actively manage your finances in Chapter 4.

But first, let’s make sure you have a solid plan to collect the money you’re earning.

Download the Full Guide to Law Firm Finances

With this guide, you’ll understand key financial concepts, financial levers affecting your business, best practices for billing and collecting money, and how to manage and outsource financial work. And, you’ll have tools to tackle business insurance and taxes.