Legal product reviews and business guidance from industry experts.

Chapter 2/6

Funding & Financing a New Law Firm

How to Start a Law Firm

9 min read

Legal product reviews and business guidance from industry experts.

Chapter 2/6

How to Start a Law Firm

9 min read

Inevitably, the first law firm financing questions we hear from lawyers are: (1) How much does it cost to start a law firm? And (2) How do I find law firm funding?

Let’s start with this: If you’re coming from a big firm, don’t apply big firm financing philosophies to your small firm. You will hemorrhage money if your first steps are to hire a huge staff, buy expensive tools, and flash out your office.

Gone are the days—especially as the world goes more remote—of needing a luxurious-feeling office space to impress your clients. In fact, we’ll wager that an accessible space is more important for a client-centered practice than a luxury office. (More on that later.)

Readjust your mindset to fund on a smaller scale.

But, before you start throwing out cash—before you start even looking for law firm funding—it’s time to get a strategy in place.

Any healthy business, including law firms, should have a written plan to forecast revenue, expenses, net profit, and cash reserves. But first, you need to understand your financial goals.

We know: You’re just starting. Who can think about five years from now? We want you to relax and dream a little. Planning your financial strategy now will help you smartly figure out the law firm funding you need to get started. You’re not locked into these numbers. They will change as you change and grow.

First, you must consider where you want your business to be in one year, three years, and five years. Once you visualize those goals, start outlining the steps to get there. These are the backbone of your financial strategy.

Hot tip: Since you’re in the beginning stages, these are wishlist numbers. You will adjust these numbers as you get a handle on your funds. Balance reality with dreams.

Ask yourself:

When you start a legal practice, you will need to spend some money at the outset—it isn’t optional. According to our experience and data over the years, $3,000 is an okay starting point. Although, $5,000 to $15,000 is more practical to have a solid footing for your first law firm. The cost depends on a wide range of variables, such as location, practice area, advertising, and more.

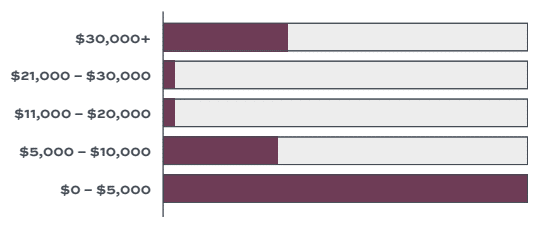

We polled members of our Lawyerist Facebook group on how much start-up capital they had when they opened their firm and they said:

Overwhelmingly, most attorneys had less than $5,000 in the bank when they started. So it’s possible, but let’s break it down.

Personal Expenses

In addition to the money needed to get your business off the ground, you’ll need to keep yourself housed and fed. It may take some time for your business to be in a solid position and pay you a salary or distribution. You should have some personal money saved to cover your living expenses for the first three to six months.

Plan for professional expenses such as licensing, continuing legal education, conferences and events, malpractice insurance, and memberships. Both licensing and legal education aren’t optional. You’ll also need different types of insurance.

The office comes first (as it is often your largest expense outside of salaries). The good news is that this is an optional expense. If the global pandemic taught us anything, it’s that you can run a firm out of your house with a desk, computer, and basic supplies. Whatever gets you started, do it. Don’t waste too much time finding the perfect office space. You can quickly get caught up in buying furniture, technology, and supplies, and soon discover that you’re drowning in minutiae and overhead.

Many more attorneys are finding success with a virtual practice. This is an excellent option to keep your overhead low. It also allows you to determine how much space you need before you lock yourself into a long-term lease. If you plan on securing a physical space, give yourself a buffer and a timeline. A standard timeline is to have a space arranged and rent money six to twelve months after starting your practice. Do whatever feels right to you.

As you purchase office supplies, only buy what you need. We’ve all gotten excited about a new space and bought fancy chairs, expensive espresso machines, art, and on and on. Buying cool office decor can be a great distraction from working on your actual business plan. Don’t fall for it!

Try to rein in the urge to make your office look expensive. If you have transparent, client-centered services and a human touch, your clients won’t care what your office looks like.

In your office space, you’ll need a computer, backup service, document scanner, and a phone or phone service.

Legal software and online services will be the tools you use the most daily in your practice. Don’t rush into buying any of these items. First, make a list of tasks you’ll need done and how you’d like those tasks to flow through the day. (We call these workflows.) We’ve all seen lawyers jump into buying new tech without figuring out how they’ll use it first.

Once you have that plan, consider:

At some point, you’ll want to think about your marketing budget, but in the beginning, it’s OK to stick to the freebies. Set up social media accounts, get referrals from friends and colleagues, and build a basic, free website with your firm’s information. When you’re ready to jump into marketing in-depth, check out our Guide to Law Firm Marketing.

Now that you know how much money you’ll need initially, let’s explore how to finance it.

To open your own firm, you’ll need some cash to cover your business’s initial expenses plus operating costs for several months. Let’s dive into how firms can fund or finance those expenses.

A line of credit is typically offered by a bank or credit union. It gives you access to money as you need it, and you can draw up to a maximum amount for a set period of time. Lines of credit are flexible, allowing you to continuously borrow the funds you pay back. You also don’t pay any interest until you borrow.

Business lines of credit are often unsecured, which means you don’t need to put forth any collateral to secure the credit. These typically come with higher interest rates, however. Lines of credit are best for short-term projects, such as office renovations or upgrading your equipment.

Credit cards are similar to lines of credit, but with a few key differences. For example, a credit card doesn’t have a draw period, so you can use it as long as the account is open. If you want actual cash in hand (like you’d receive from your line of credit), you’ll need to perform a cash advance on your card. This often comes at extremely high-interest rates, which can cost you.

Speaking of high interest rates, credit cards come with higher rates than the other lending options listed here. With some cards, you may be able to pay the balance off each month and avoid interest charges. That makes them an often ideal choice for day-to-day spending within your firm.

Small business loans are tailored specifically for business owners just getting started. In general, we recommend avoiding small business loans for law firm financing or funding. Typically, these loans require you to leverage your own home or other assets to secure it, bringing a fair amount of risk to the table.

Loans from friends or family may come with the added benefit of a low-interest rate. But they can also come with strings attached that can strain a relationship if you don’t pay it back on time. Before you reach out for help from a friend or family member, seriously weigh your comfort level with the relationship.

Although credit cards and loans are available, you should only use them if you are confident in your profitability. If you can demonstrate that you will have the cash later, access the credit if you need. If you’re not sure when you’ll have the money to pay your debts, though, accessing credit or loans may not be the best option for your firm.

Have a handle on the basics of law firm funding and financing? Then let’s move to your next step: your new law firm business plan.

Download the Full Guide on How to Start a Law Firm

With this guide, you’ll have the tools to plan, strategize, organize, finance, brand, launch, market, and run a new firm.